Impact of carbon pricing on market valuation of european listed companies

- Vincent Auriac

- Feb 8

- 4 min read

December 2022

We studied the stock market consequences of carbon pricing on the largest listed

companies in Europe.

Faced with the systemic risk posed by climate change, taking into account so-called “extra-

financial” criteria is now essential. Investors must be able to identify and measure these

risks in order to protect the long-term profitability of their investment.

The initial observation is as follows : the externalities (hidden costs) linked with CO2

emissions are not borne by the company even though it emits them. Is our economic

model still relevant in a warming world and where climate damage appears month after

month to be higher than the financial wealth created ?

What would happen if Nature sent companies the bill for the damage it suffered ? What

would be the consequences on their stock market valuation ?

Methodology

We capture all company's CO2 emissions across its entire value chain (scope 1, 2 and 3

upstream and downstream¹), provided by Trucost². We estimate scope 3 for certain

sectors such as banks when they do not publish this information.

We convert CO2 emissions into euros. Research by climate economists, taken up by the

IPCC³, values a ton of CO2 at 113 euros. This is a level higher than the €66 price of the EU

ETS CO2 quota in October 2022 and much higher than other world prices. This is the

carbon price necessary to meet the ambitious trajectory of +1.75°C, in accordance with

the Paris Agreements⁴

.

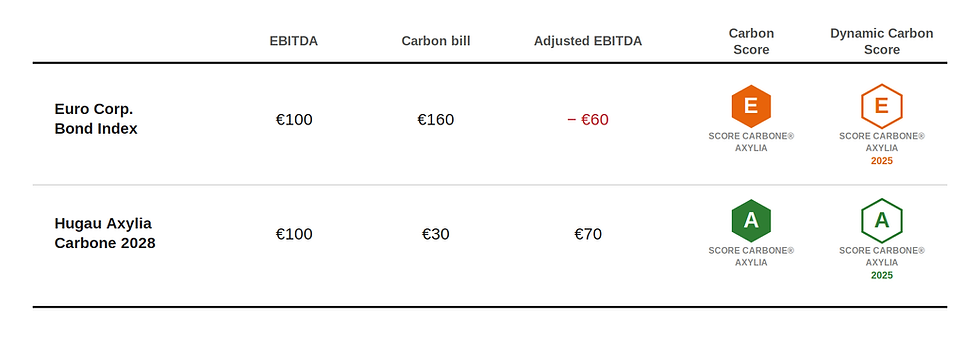

We thus obtain a valuation in euros of the carbon impact of the company on Nature : the

carbon bill. This amount is then subtracted from the company's operating profit (EBITDA).

It is from this calculation that we then obtain the new market capitalization of each

company, corrected for the cost of the carbon it emits (by multiplying the adjusted EBITDA

by the capitalization multiple before adjustment).

Results with a carbon price of 113 euros per ton of CO2

This methodology was applied to the 600 largest European stock market capitalizations.

If companies had to bear a carbon price of €113 per tonne of CO2 on their scope 1 and 2

only, the European stock market valuation would decrease by 13.3%.

If companies had to bear this price on all of their CO2 emissions (scopes 1, 2 and 3), the

reduction would be 53.7%

Scope 3 is often underestimated, or even not reported by companies. However, scope 3

represents on average 80% of their greenhouse gas emissions (source CDP⁵). This is why it

is essential to take it into account.

Our approach measures a company's carbon-related financial risk, in order to reveal its

exposure to CO2 across its entire value chain and its financial risk if carbon were to be

priced. In this case, it becomes very vulnerable by integrating emissions from its scope 3,

the most important of all three.

We note that by imposing a price on all scopes, the impact on valuation is more than 3

times higher than if we only took into account scopes 1 and 2.

Impact of a carbon price of 200 euros per ton of CO2

The IPCC scenarios estimate that in 2030, the price of a ton of CO2 should reach 200

euros to align with the Paris Agreement. We therefore made the same calculations by

using this price. We are seeing an even greater decline in stock market valuation.

With a carbon cost of €200 per ton of CO2 on scopes 1 and 2, the European stock market

valuation would decrease by 17.4%.

If companies had to bear this cost on all of their emissions (scope 1, 2 and 3), the

reduction would be 63%.

Conclusions

Climate change represents a real threat to the valuation and financial stability of

companies. As climate risks become more and more pressing, it is becoming essential to

take them into account when evaluating companies. The market does not yet take into

account the cost of companies' CO2 emissions in their valuation.

The Axylia study shows that taking into account the cost of carbon leads to a reduction

between 13% to 63% in the stock market valuation of European companies. This

represents a loss of valuation of more than €4,500 billions.

Global warming will lead to increasingly drastic consequences, whether it be new

government regulations or new consumption patterns. These decisions could cause

serious difficulties for companies highly exposed to carbon which have not taken this

major risk into account. Investors run the risk of severe depreciation of their financial

assets in the next 10 years if they do not anticipate it now.

Notes

¹ CO2 emissions can be classified into three categories: direct greenhouse gas emissions (Scope 1), indirect energy-related emissions (Scope 2) and other indirect emissions (Scope 3)

² Trucost, a subsidiary of Standard and Poor's, is a pioneer in researching and calculating the carbon footprint of companies

³ Intergovernmental Expert Group on Climate Change : https://www.ipcc.ch/

⁴ The Paris Agreement is an international treaty which sets the objective of keeping the rise in global temperature below +2°C

⁵ Carbon Disclosure Project : https://www.cdp.net/en

Comments